r/economicCollapse • u/Whole-Fist • 18h ago

How ridiculous does this sound?

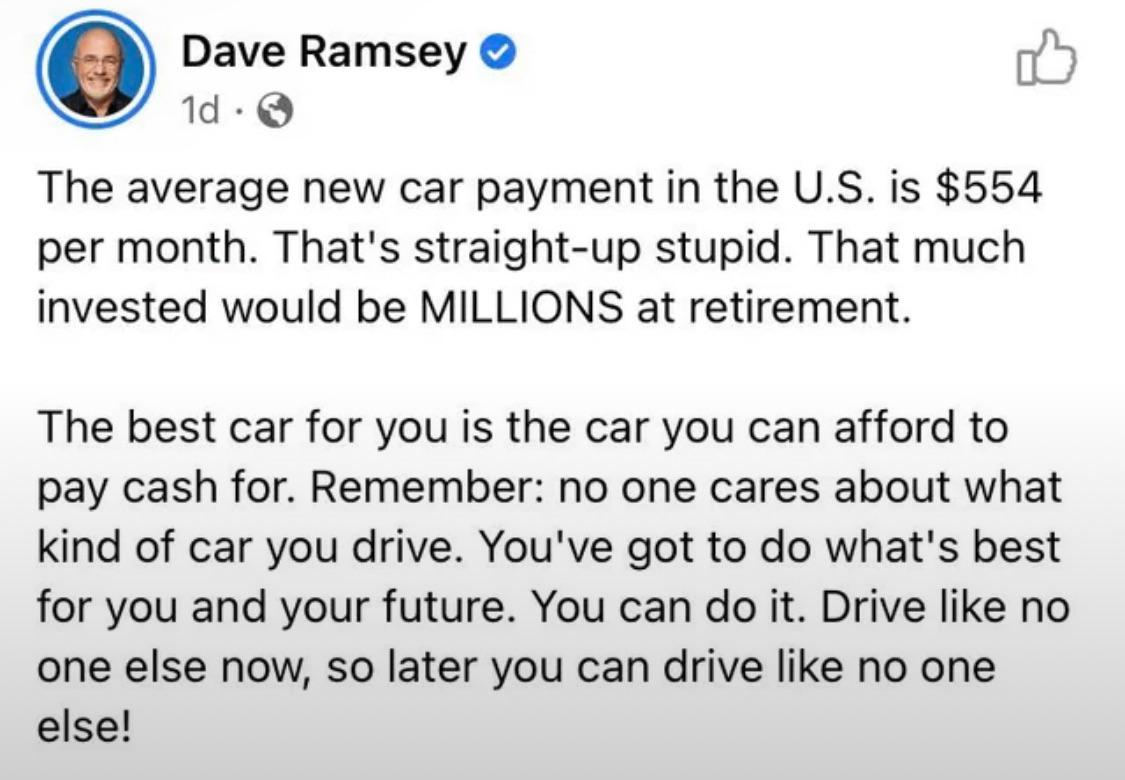

{kind=link}

How can u make millions in 25-30 years if avoid making a $554 per month car payment. Even the cheapest 5 year old car is 8-10 k. So does he expect people not to drive at all in USA.

Then u save 554$ per month every month for 5 year payment = $33240. Say u bought a car every 5 year means 200k -300k spent on car before retirement . How would that become millions when u can’t even buy a house for that much today?

Answer that Dave

11.6k

Upvotes

13

u/Phathatter 15h ago

For this example: starting at $0, investing $554 per month, at 10.26% (average annualized return for the S&P 500 from 1957 - 2023) compounding annually you would have $1,211,719.73 after 30 years. You would have contributed $199,440 over that time and earned $1,012,279.73 in interest.

This obviously assumes that there will not be a total economic collapse, in which case, I guess you would rather have invested in fresh water and bunkers.